Due Diligence Documents: A Startup Founder's Guide

Unlock essential insights into due diligence documents for startups. Learn how to prepare effectively and impress investors with your readiness.

July 18, 2026 · 10 min read

Due diligence documents are the records and data that investors review to verify a business’s financial health, legal standing, operations, and ownership before committing capital. Think of them as the evidence file that turns your pitch deck’s claims into provable facts. A comprehensive mid-market file spans 200–400 documents across seven workstreams, with the detailed review phase lasting 8–10 weeks after a letter of intent. That scope surprises most first-time founders. Getting organized before investors ask is the single most effective way to protect deal momentum and signal that your company is ready to be owned by someone else.

What are the essential due diligence documents investors request?

Investors organize their requests into seven primary workstreams. Each workstream covers a distinct area of business risk, and the depth of each one scales with deal size and deal type. A seed round might require a fraction of what a Series B or an acquisition demands, but the categories stay the same.

| Workstream | Key documents |

|---|---|

| Financial | Audited financials, management accounts, cap table, revenue forecasts, debt schedules |

| Legal and regulatory | Certificate of incorporation, shareholder agreements, board minutes, licenses, permits |

| Commercial | Customer contracts, pipeline reports, market analysis, pricing schedules |

| Operational | Org chart, supplier agreements, lease agreements, insurance policies |

| People and integrity | Employment contracts, option grants, background checks, compensation structure |

| Technology and IP | Patent filings, software licenses, IP assignment agreements, security audits |

| ESG | Environmental policies, governance documents, diversity reporting |

The financial workstream is where most investors start. Audited financials, a clean cap table, and a detailed revenue model tell investors whether your numbers hold up under scrutiny. The legal workstream follows closely, covering everything from your certificate of incorporation to any threatened litigation. Missing or unsigned IP assignment agreements are one of the most common deal-killers in technology startups, because investors need to confirm the company actually owns what it sells.

People and integrity screening is treated as a non-negotiable fourth pillar by institutional investors, sitting alongside financial, legal, and operational diligence. That means background checks on founders and key executives, not just employment contracts. Investors want to know who they are backing, not just what the business does.

The scope of your due diligence checklist also depends on the deal structure. A seed round from an angel investor might require only a term sheet, cap table, and basic financials. A Series B from an institutional fund will demand audited statements, detailed customer contracts, and a full IP audit. An acquisition adds a closing binder, representations and warranties, and indemnification schedules on top of everything else.

How should startups organize and prepare for investor review?

The structure of your data room communicates as much as its contents. A well-maintained data room with clear folder structure and consistent naming signals operational maturity to investors. Disorganized files, by contrast, raise immediate doubts about how well you run the business day to day.

A practical folder structure mirrors the seven workstreams above. Each top-level folder carries the workstream name. Subfolders break documents into logical groups, such as “01_Audited_Financials” or “03_Customer_Contracts_Active.” Version control matters too. Label every document with a date or version number so investors always know which file is current. Never let two versions of the same document sit in the same folder without clear labels.

Pro Tip: Aim to have at least 80% of required documents organized in your virtual data room before you start fundraising. Gaps discovered mid-process slow everything down and signal unpreparedness to investors who are already evaluating multiple deals.

Timing is the underrated variable in document preparation. Founders who wait until an investor asks for a data room lose two to four weeks scrambling to gather files. Founders who build the room in parallel with their pitch deck enter conversations from a position of strength. You can share a link, answer questions in real time, and focus your energy on the relationship rather than the paperwork.

Proactive disclosure is the other discipline that separates prepared founders from reactive ones. Negative documents like threatened litigation or customer concentration must be disclosed with remediation plans attached. Investors expect imperfection. They do not expect surprises. A clean explanation of a known issue builds trust. A hidden issue discovered during review destroys it.

For a deeper look at building a secure, well-structured room, the BabyLoveRaise guide to secure data rooms covers the practical setup steps for technology startups heading into a funding round.

Which documents and issues commonly raise red flags?

Red flags in business due diligence fall into two categories: structural problems that reflect how the company was built, and disclosure problems that reflect how the founder is behaving in the process. Both can kill a deal.

The most common structural red flags include:

- Inconsistent cap tables. If your cap table does not reconcile with your shareholder agreements and board minutes, investors cannot confirm who owns what. This is a fundamental legal problem.

- Missing IP assignments. Founders who wrote code or developed products before formally assigning those assets to the company leave a gap that acquirers and institutional investors will not accept.

- Customer concentration. A single customer representing more than 30% of revenue is a material risk. Investors will discount valuation or add earnout provisions to account for it.

- Unresolved litigation. Any threatened or pending legal action must be disclosed with a clear status update and legal counsel’s assessment of exposure.

- Unsigned or expired contracts. Verbal agreements and expired customer contracts do not survive legal due diligence. Investors need executed, current agreements.

Due diligence is a defensive narrative. Even negative information should be accompanied by transparent explanations or remediation plans to maintain trust and keep the deal moving forward.

Disclosure problems are often more damaging than the underlying issues themselves. An investor who discovers a problem you did not disclose will question everything else in the room. Management interviews and site visits are as important as documents in forming investors’ understanding of a business. How you answer hard questions in person carries as much weight as what your files contain.

Financial statement red flags include revenue recognition inconsistencies, unexplained spikes in accounts receivable, and gross margin compression that does not match your narrative. These are not always signs of fraud. They are often signs of sloppy accounting. Either way, they require clear explanations before investors will proceed.

What is the due diligence process timeline?

The investment due diligence process runs in three phases, each with distinct document requirements and decision gates.

-

Preliminary diligence (pre-LOI). Investors review your pitch deck, a teaser, basic financials, and a high-level cap table. The goal is to decide whether to issue a letter of intent. This phase is light on documents but heavy on narrative. Your pitch deck and one-pager carry most of the weight here.

-

Detailed diligence (8–10 weeks post-LOI). This is the full document review phase, covering all seven workstreams. Investors work through your virtual data room, submit written questions, and schedule management presentations. Most deals stall or die in this phase due to document gaps or undisclosed issues.

-

Confirmatory diligence (final 2 weeks before closing). Investors re-verify bank statements, confirm key employee retention, and check that no material change has occurred since the LOI. This phase is about confirming what was already agreed, not discovering new information.

Pro Tip: Build a closing binder of all final signed documents and update it in real time throughout the process. Last-minute scrambles to locate executed agreements are one of the most common causes of closing delays.

A structured, phased timeline with clear document owners inside your team avoids duplication of effort. Assign one person to own each workstream folder. That person is responsible for completeness, version control, and responding to investor questions in that area. Without clear ownership, documents get duplicated, outdated versions circulate, and investors lose confidence in the process.

The management presentation, typically scheduled in weeks three to five of detailed diligence, is your opportunity to walk investors through the business in person. Prepare a structured deck that mirrors the workstream categories. Anticipate the hard questions on customer concentration, IP ownership, and key person risk before they are asked.

Key Takeaways

Comprehensive, well-organized due diligence documents are the single most effective way to protect deal momentum, build investor trust, and prevent valuation discounts during a funding round or acquisition.

| Point | Details |

|---|---|

| Seven workstreams cover all risk areas | Financial, legal, commercial, operational, people, technology, and ESG documents form the complete picture. |

| 80% readiness before fundraising | Organize the majority of your data room before investor conversations begin to avoid losing momentum. |

| Proactive disclosure builds trust | Disclose known issues with remediation plans attached; surprises discovered mid-review damage credibility far more than the issues themselves. |

| Three-phase timeline governs the process | Preliminary, detailed (8–10 weeks), and confirmatory (2 weeks) phases each have distinct document requirements. |

| Closing binder prevents last-minute delays | Maintain a real-time updated file of all final signed documents throughout the process, not just at the end. |

The part founders get wrong about due diligence

Most founders treat due diligence as a compliance exercise. Get the documents together, hand them over, and wait. That framing costs deals.

Due diligence is risk mitigation and valuation validation. It surfaces deal-killing issues early enough to address them. The founder who understands that is the one who builds the data room six months before fundraising, not six days after the term sheet arrives. I have watched founders with genuinely strong businesses lose deals because their cap table had a rounding error that took three weeks to reconcile. The business was fine. The process was not.

The other thing founders underestimate is the people dimension. Investors are not just buying your product or your revenue. They are betting on you and your team. How you show up during diligence, how you answer hard questions, how you handle a request for a document you do not have, all of that is data. A due diligence checklist helps you focus on what matters most rather than drowning in paperwork, but the checklist is a floor, not a ceiling.

My honest advice: treat your data room as a living document, not a one-time project. Update it quarterly. Add new contracts as they are signed. Archive old versions cleanly. When an investor asks for access, you send a link in ten minutes, not ten days. That speed alone signals something important about how you run your company.

— Paul

How BabyLoveRaise fits into your fundraising process

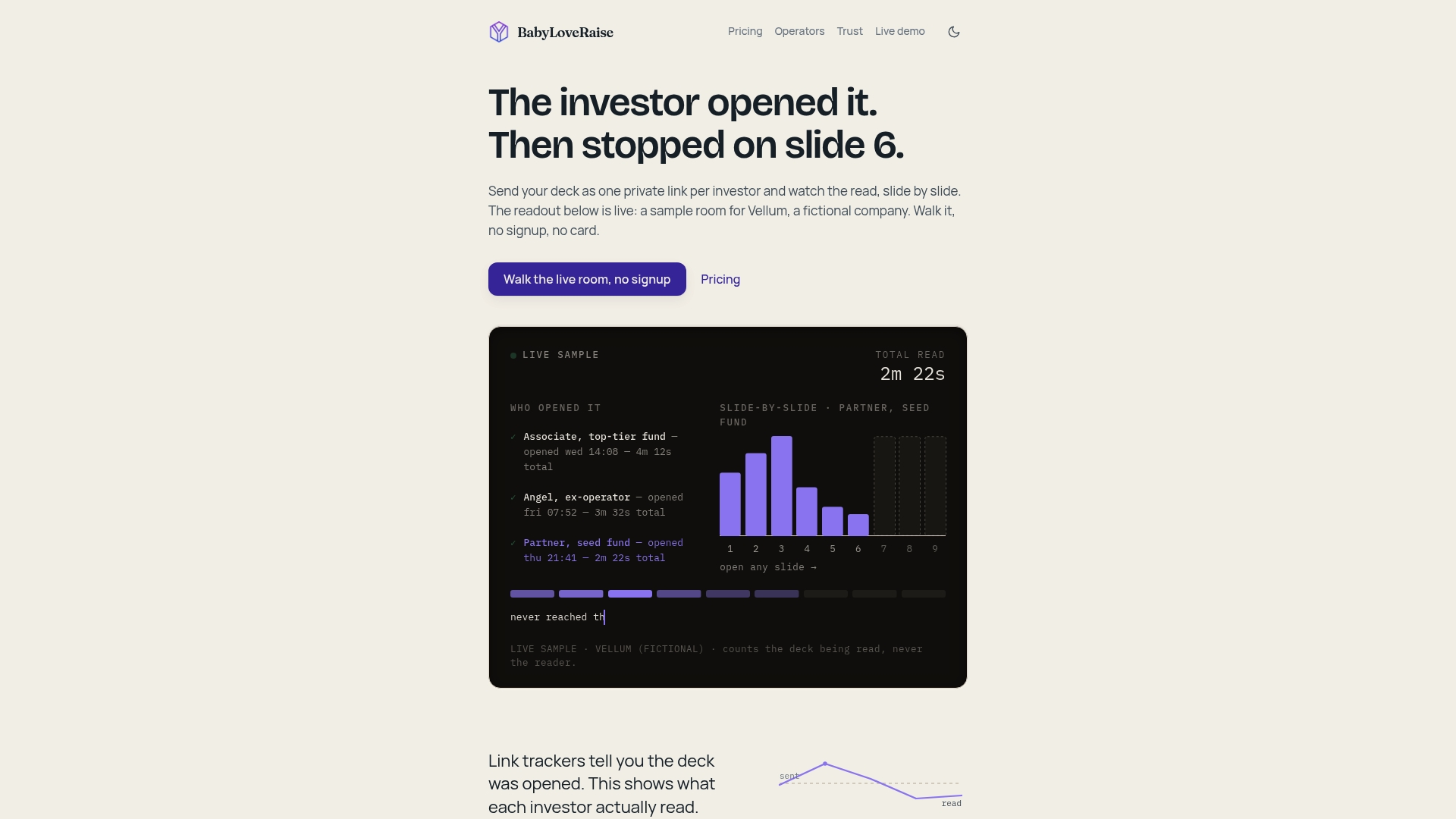

Organizing your pitch deck and tracking investor engagement is the front end of the same process that leads to a full data room review. BabyLoveRaise gives founders a hosted raise room where every investor interaction with your deck is recorded: who opened it, which slides they read, and where attention dropped off.

That per-slide engagement data tells you which parts of your story are landing and which need work before investors get to the due diligence stage. BabyLoveRaise is priced per raise rather than per seat, which means the cost scales with your actual fundraising activity. The platform also converts your raise room into a permanent archive when the round closes, so your records stay intact without a recurring subscription. For founders who want to understand how their documents and decks are being received, the trust and security details are publicly listed on the BabyLoveRaise website.

FAQ

What are due diligence documents?

Due diligence documents are the records, contracts, and financial data that investors or acquirers review to verify a company’s claims before closing a deal. They typically span seven workstreams including financial, legal, commercial, operational, people, technology, and ESG.

How many documents does a typical due diligence process require?

A mid-market investment due diligence file typically includes 200–400 documents across all workstreams. Seed rounds require far fewer, while M&A transactions demand the full scope.

How long does the due diligence process take?

The detailed diligence phase runs 8–10 weeks after a letter of intent is signed, followed by a two-week confirmatory phase before closing. Preliminary diligence before the LOI can add several additional weeks depending on investor pace.

What is a virtual data room and why does it matter?

A virtual data room is a secure, organized digital repository where founders store and share due diligence documents with investors. A clean, well-structured room signals operational maturity and reduces investor skepticism. The BabyLoveRaise VDR guide covers the setup process in detail.

What are the most common red flags in due diligence?

The most common red flags are inconsistent cap tables, missing IP assignments, undisclosed litigation, and customer concentration above 30% of revenue. Each of these requires a clear explanation and, where possible, a documented remediation plan before investors will proceed.