How Investor Relations Work: A Startup Founder's Guide

Learn how investor relations work and why it's crucial for startups. Enhance credibility and secure funding with effective IR strategies.

July 14, 2026 · 10 min read

Investor relations (IR) is defined as a strategic management discipline that integrates finance, communication, marketing, and securities law compliance to enable effective two-way communication between a company and its investors. For startup founders and business leaders, understanding how investor relations work is not optional. IR directly shapes how the market values your company, how investors perceive your credibility, and whether your next funding round closes on your terms. Regulatory frameworks like the Sarbanes-Oxley Act and securities disclosure laws make IR a compliance obligation as much as a communication strategy. The earlier you build IR discipline into your company, the stronger your position at every stage of growth.

How investor relations work: the core functions

IR is not a single activity. It is a system built on three pillars: communication, engagement, and risk preparedness.

Communication covers every financial disclosure, regulatory filing, and narrative your company puts in front of investors. The equity story sits at the center of this pillar. Your equity story is the consistent, auditable narrative that explains what your company does, why it wins, and how it creates value for shareholders. Best-in-class IR functions maintain this story consistently across every external touchpoint, from earnings calls to pitch decks to press releases. Inconsistency in that narrative is one of the fastest ways to lose investor confidence.

Engagement covers targeted outreach, roadshows, and direct meetings with investors and analysts. Effective engagement is not broadcasting. It is a two-way exchange where you learn what investors believe about your company and correct misperceptions before they affect your valuation. Roadshows, one-on-one meetings, and investor days all serve this function.

Risk preparedness is the pillar most founders ignore until it is too late. IR extends into crisis management, working alongside corporate secretary and legal teams to stabilize share price during adverse events like management changes, product failures, or market downturns. Prepared crisis communication playbooks are not a luxury. They are a core IR deliverable.

Pro Tip: Write your crisis communication playbook before you need it. Define who speaks, what they say, and through which channels. A playbook drafted under pressure is a playbook full of mistakes.

IR organizational structure

IR typically operates as a dedicated department reporting to the CFO, with direct lines to the CEO and Board. In smaller companies and early-stage startups, IR is often outsourced to a fractional IR professional or advisory firm. The U.S. Department of Labor classifies IR as specialized public relations requiring both finance and legal expertise. That classification matters because it signals the skill set required. IR is not a marketing function wearing a finance hat. It requires genuine fluency in securities law, financial modeling, and stakeholder communication.

How does IR support startup growth and fundraising?

IR becomes critical the moment you take outside capital. The discipline does not begin at IPO. It begins at your first institutional raise.

-

Establish transparency from day one. IR professionals involved early in IPO, SPAC, or M&A processes build trust through consistent communication and regulatory compliance. Founders who treat early investors as partners rather than check-writers build the kind of credibility that survives a pivot or a missed quarter.

-

Manage investor expectations proactively. Valuation gaps almost always trace back to a communication failure. When investors do not understand your capital allocation priorities or your growth model, they fill the gap with assumptions. Those assumptions are rarely favorable.

-

Communicate strategic priorities clearly. Every fundraising round is a chance to sharpen your equity story. Use IR discipline to align your pitch deck, your financial model, and your verbal narrative into one coherent message. Investors compare what you say in meetings with what they read in your materials. Gaps between those two create doubt.

-

Handle setbacks through the IR framework. A product launch delay or a revenue miss is not automatically fatal to investor confidence. What damages confidence is silence or inconsistency. IR gives you the framework to communicate bad news in a way that preserves credibility. Acknowledge the issue, explain the cause, and state the corrective action clearly.

-

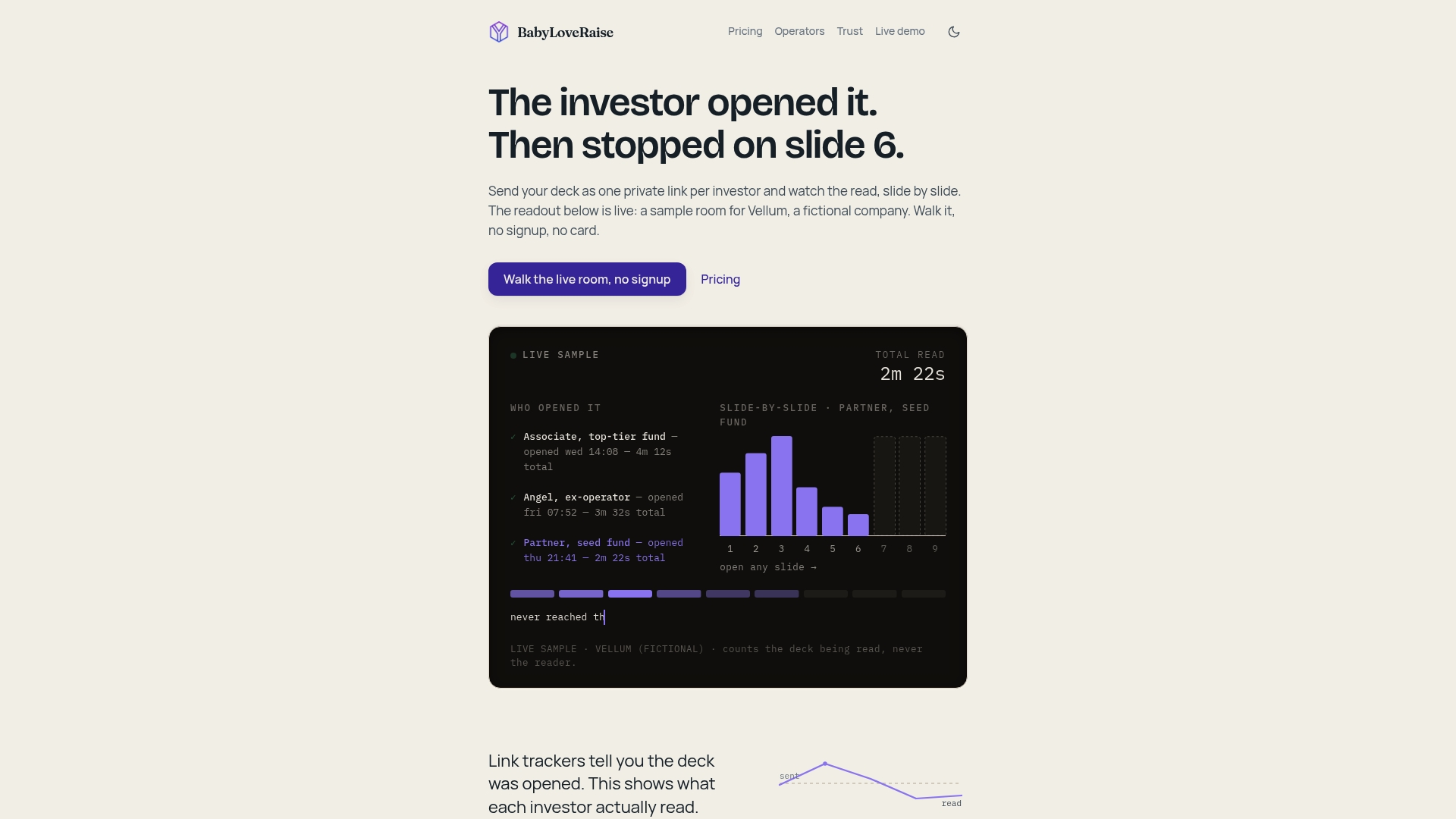

Use IR data to guide follow-up. Knowing which investors engaged with your materials, which slides held their attention, and which ones they skipped tells you where your narrative is working and where it is not. That feedback loop is the difference between a reactive fundraise and a managed one.

What are the best practices for managing investor relations?

The most effective IR programs are built around objectives, not activities. Shifting from activity-based to objective-based IR planning produces measurable improvements in shareholder engagement and communication effectiveness. Counting meetings held is not IR strategy. Identifying specific shareholder gaps and closing them is.

Maintain a canonical equity story

Your equity story must exist as a single, audited document. Every external communication, from your website to your investor deck to your LinkedIn posts, should trace back to that document. Leading firms audit their equity story regularly to prevent drift and conflicting information. Assign one person ownership of the canonical version and require sign-off before any external material goes live.

Use CRM tools and AI-assisted meeting prep

AI-assisted meeting preparation integrated with CRM history helps IR teams anticipate analyst questions and prepare management commentary that supports model updates without ambiguity. This is not about replacing human judgment. It is about arriving at every investor meeting with the full context of that relationship already loaded. Know what the investor asked last time, what they pushed back on, and what they care about most.

Conduct annual perception studies

Annual perception studies measure investor sentiment and messaging effectiveness over time. They reveal whether your equity story is landing as intended or whether the market has formed a different view of your company. Most startups skip this step entirely. That is a mistake. Perception studies give you the data to refine your communication strategy before a valuation gap becomes a funding problem.

Align retail and institutional communication

Retail investors require clear, accessible communications aligned with formal disclosures. Digital FAQs, plain-language updates, and webinars serve retail audiences without creating separate information channels that conflict with regulatory filings. Consistency across both audiences is not just good practice. It is a regulatory obligation.

Pro Tip: Build a simple IR calendar at the start of each quarter. Map every planned disclosure, meeting, and external communication against your equity story. Gaps in that calendar are gaps in your investor narrative.

| IR approach | What it measures | Outcome |

|---|---|---|

| Activity-based planning | Meetings held, presentations delivered | Tracks effort, not results |

| Objective-based planning | Shareholder gaps closed, sentiment shifts | Tracks outcomes and communication effectiveness |

| Perception studies | Investor sentiment, messaging accuracy | Reveals gaps between intended and received narrative |

| CRM-integrated engagement | Meeting history, investor priorities | Improves preparation and follow-up quality |

What are the common challenges in investor relations?

Every IR program faces predictable obstacles. Knowing them in advance is the only way to avoid them.

-

Equity story drift. Over time, different team members describe the company differently. Sales decks diverge from investor decks. Website copy drifts from earnings call language. Inconsistent messaging across materials confuses investors and signals internal misalignment. The fix is a single canonical equity story with enforced version control.

-

Retail investor invisibility. Founders often focus entirely on institutional investors and ignore retail shareholders. Retail investors who feel uninformed become vocal critics. Plain-language updates and accessible digital channels solve this without creating compliance risk.

-

Selective disclosure risk. Sharing material information with one investor before others is a securities law violation. Every IR communication must be designed with Regulation FD in mind. When in doubt, disclose publicly first.

-

Crisis unpreparedness. Most startups have no crisis communication plan. When a negative event hits, the absence of a plan forces improvised responses that often make the situation worse. A prepared playbook, reviewed by legal counsel, is the baseline.

-

Internal misalignment. Finance, communications, and legal teams often operate in silos. IR requires all three to move together. A disclosure approved by finance but not reviewed by legal is a liability. Build cross-functional review into every material IR communication.

-

Overreliance on technology. AI and CRM tools improve efficiency in investor engagement, but they do not replace accurate disclosure. Technology supports IR. It does not substitute for the judgment and consistency that build long-term credibility.

Key Takeaways

Investor relations works when it integrates consistent communication, targeted engagement, and crisis preparedness into a single, objective-driven program that builds investor confidence at every stage of a company’s growth.

| Point | Details |

|---|---|

| IR is a discipline, not a task | Combine finance, communication, and compliance into one coordinated program from your first raise. |

| Equity story consistency is non-negotiable | Audit every external material against a single canonical narrative to prevent investor confusion. |

| Objective-based planning outperforms activity tracking | Measure shareholder gaps closed and sentiment shifts, not meetings held. |

| Crisis playbooks belong in every IR program | Prepare crisis communication frameworks before an adverse event forces improvised responses. |

| Engagement data sharpens follow-up | Knowing which investors read your materials and where attention dropped makes every follow-up more targeted. |

What I’ve learned about IR that most founders find out too late

Founders consistently underestimate how early IR discipline pays off. The instinct is to treat investor communication as something you formalize after a Series B. That instinct is wrong.

Transparency is the core confidence-building tool in IR, not polish. Investors do not expect perfection. They expect honesty and consistency. A founder who communicates a setback clearly and with a plan recovers faster than one who goes quiet and hopes the problem resolves itself. I have seen both approaches play out, and the difference in investor trust is not subtle.

The other mistake I see constantly is treating the equity story as a pitch deck rather than a living document. Your pitch deck is one output of the equity story. The story itself must exist independently, get updated when the business changes, and get audited before any external communication goes out. Founders who skip that discipline end up with five different versions of their company story floating in the market, and investors notice.

The shift from activity-based to objective-based IR planning is the single most practical change a founder can make. Stop counting investor meetings. Start tracking which specific gaps in shareholder understanding you closed this quarter. That reframe changes how you prepare for meetings, how you measure success, and how you allocate time across your IR program.

— Paul

How BabyLoveRaise fits into your IR workflow

Knowing which investors actually read your deck changes everything about how you manage follow-up and refine your narrative.

BabyLoveRaise gives founders a hosted raise room that records per-slide engagement, so you know who opened your deck, which slides held attention, and which ones got skipped. That data turns two identical silences, “never opened it” and “read everything and passed,” into two different states with two different responses. Follow-ups go to actual readers. Deck revisions target the slides where attention dropped. For founders building IR discipline from the ground up, that feedback loop is the kind of signal that used to require a co-founder or an IR advisor in the room. Check the BabyLoveRaise pricing page to see plans built around the raise, not a per-seat subscription that outlasts your round.

FAQ

What is investor relations in simple terms?

Investor relations is the function that manages communication between a company and its investors. It combines financial disclosure, regulatory compliance, and targeted engagement to support fair market valuation.

When should a startup start building investor relations?

IR discipline should begin at the first institutional raise, not at IPO. Early transparency and consistent communication build the credibility that supports every subsequent funding round.

What is the role of investor relations during a fundraise?

IR ensures that your equity story, pitch materials, and verbal narrative align consistently. It also manages investor expectations, tracks engagement, and prepares the team to handle setbacks without losing credibility.

How do you manage investor relations without a dedicated team?

Founders without a dedicated IR team should maintain a single canonical equity story, use a CRM to track investor interactions, and prepare a basic crisis communication plan. Fractional IR advisors and tools like BabyLoveRaise can fill the gap without the cost of a full-time hire.

What is the biggest mistake founders make in investor relations?

The most common mistake is treating IR as a reactive function. Founders who communicate only when they have good news lose credibility the moment something goes wrong. Proactive, consistent communication is the foundation of every effective IR program.